Mastering Design Thinking at MIT

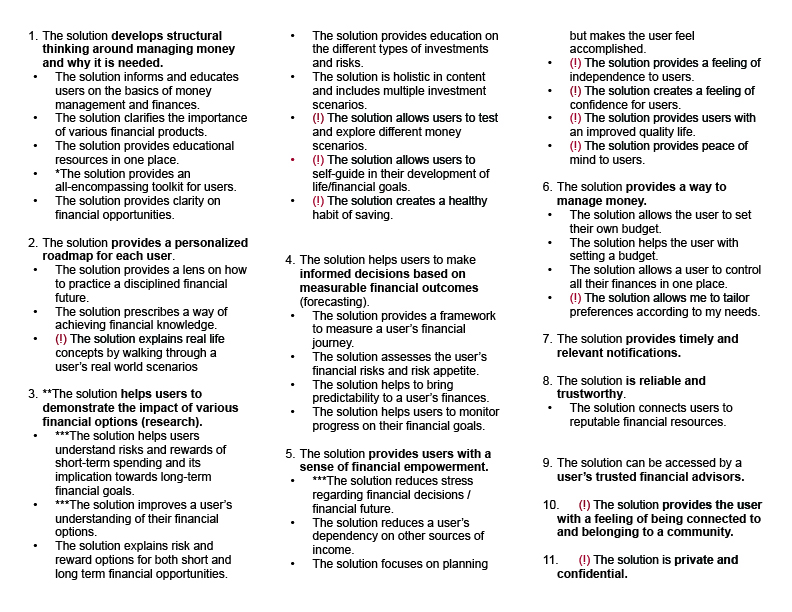

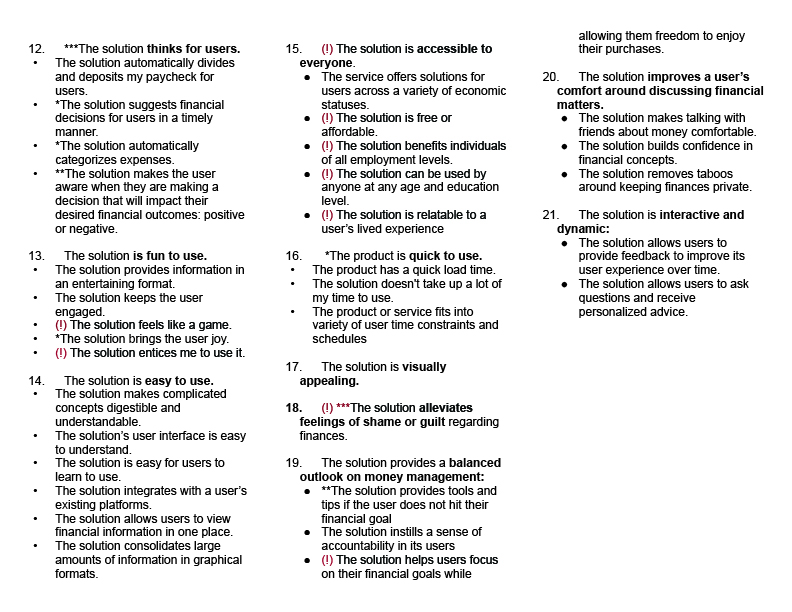

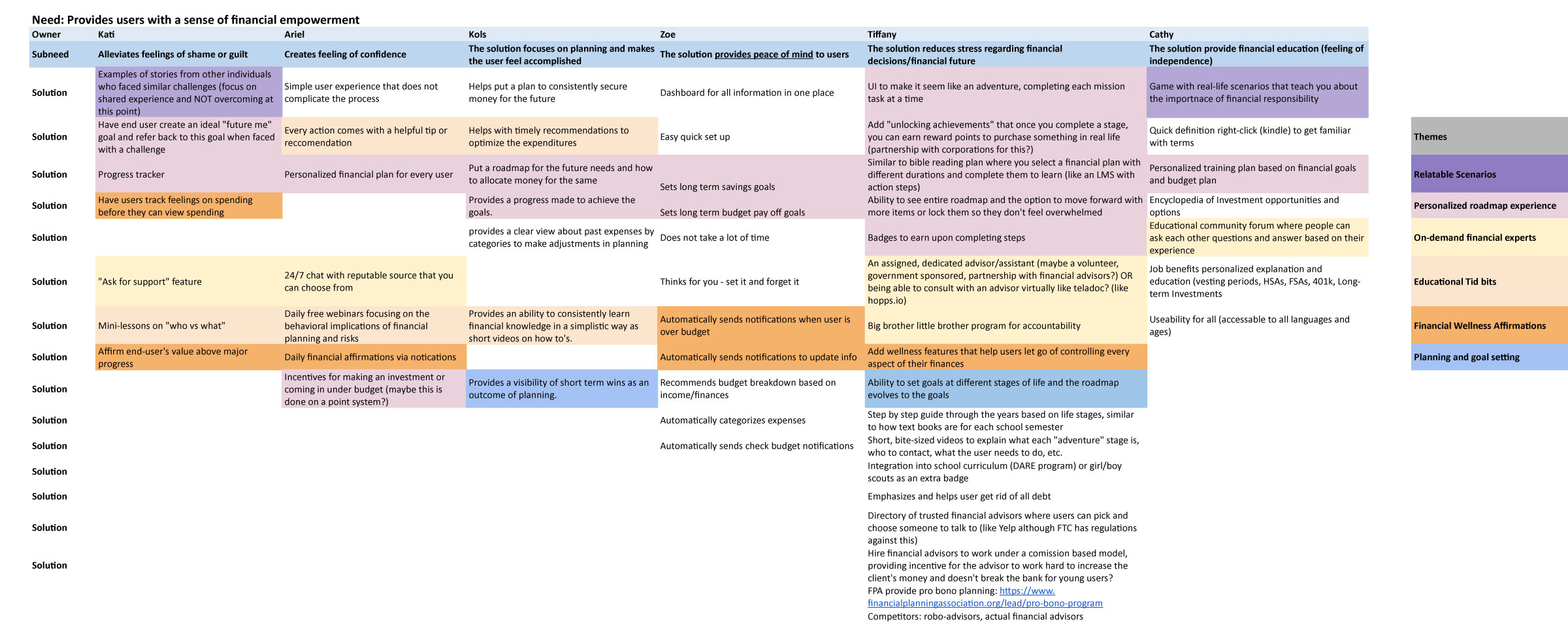

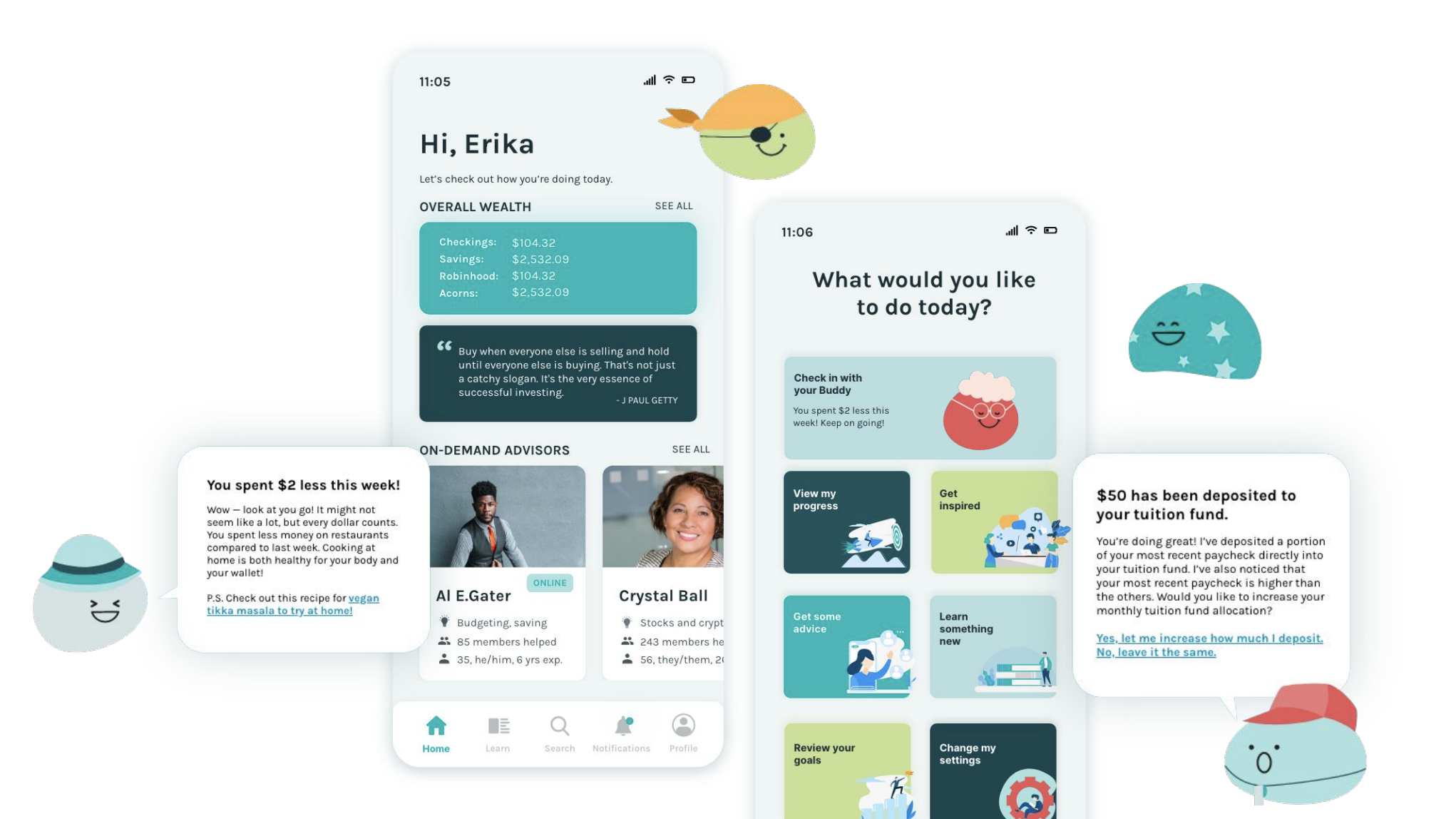

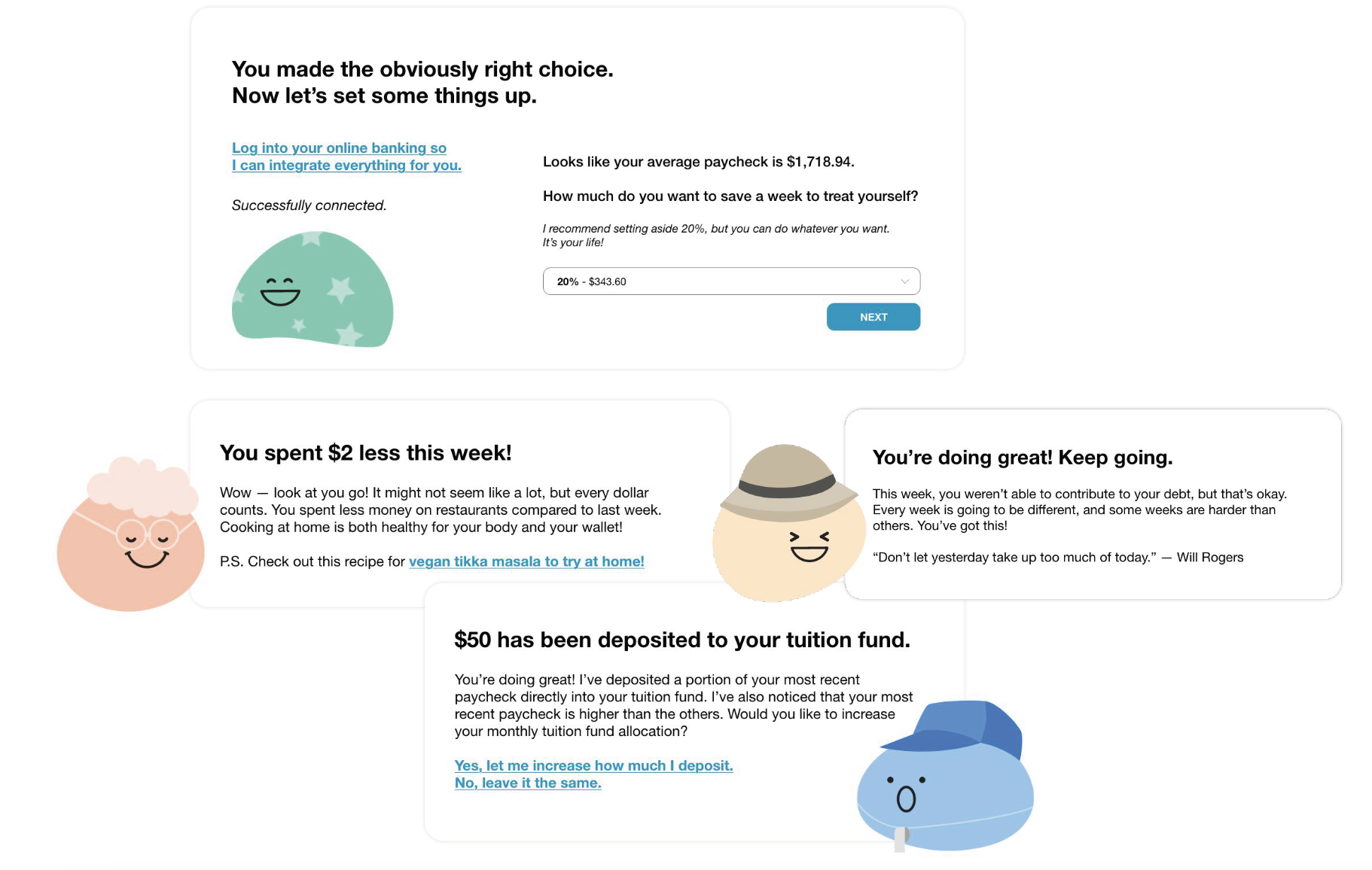

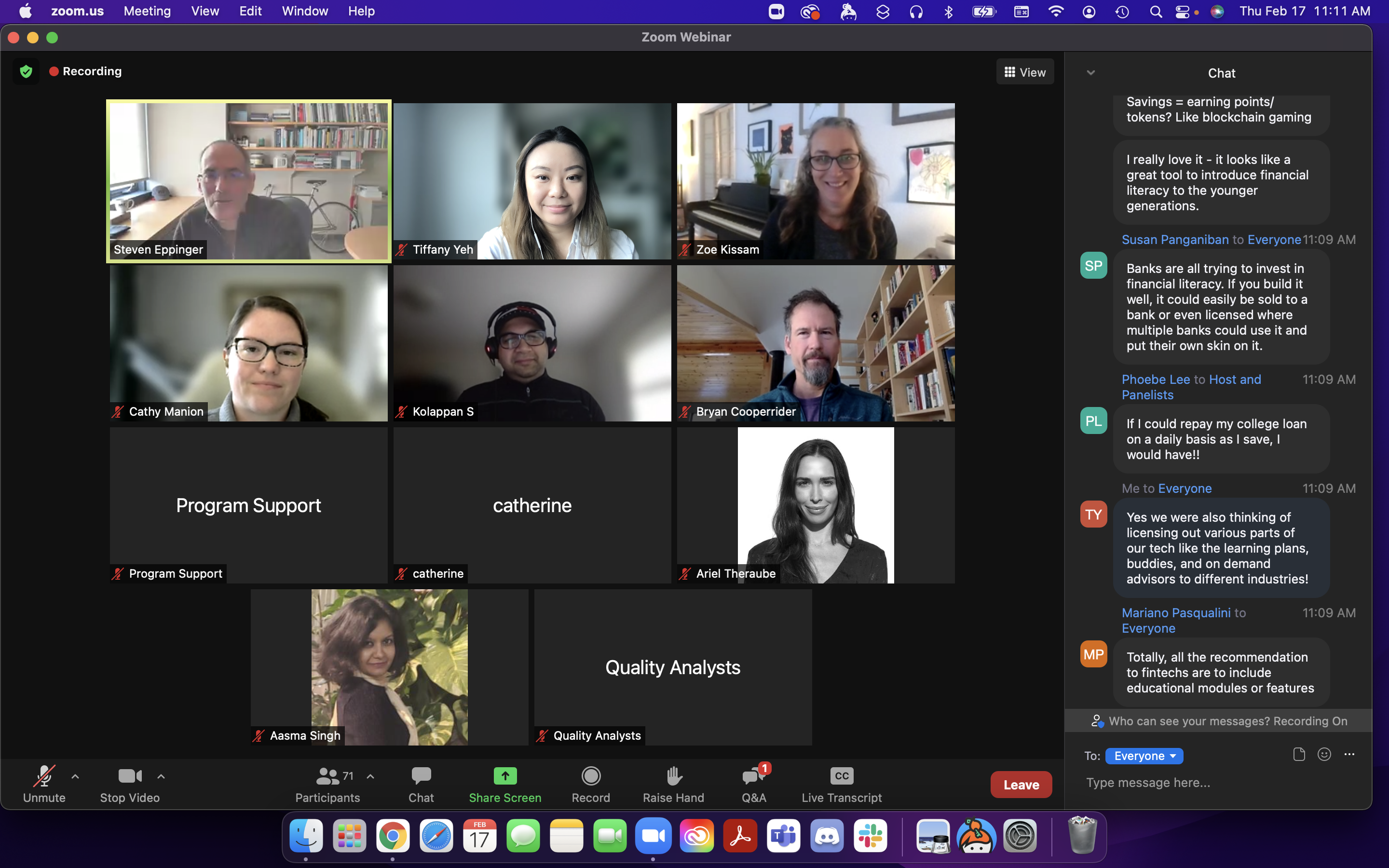

I worked with a team of 5 talented professionals to come up with a solution that would improve financial literacy in young adults. My personal contributions to the project were designing the app solution, designing the pitch deck, and coming up with the winning idea of AI helper bots.

The 6-month program, Mastering Design Thinking at MIT, involved:

- conducting interviews/user research

- identifying primary, secondary, and latent needs;

- creating service experience cycle and customer journey maps

- discovering real, winnable opportunities

- appling the design for environment (DFE) and life cycle assessment (LCA) principles to the product design process.

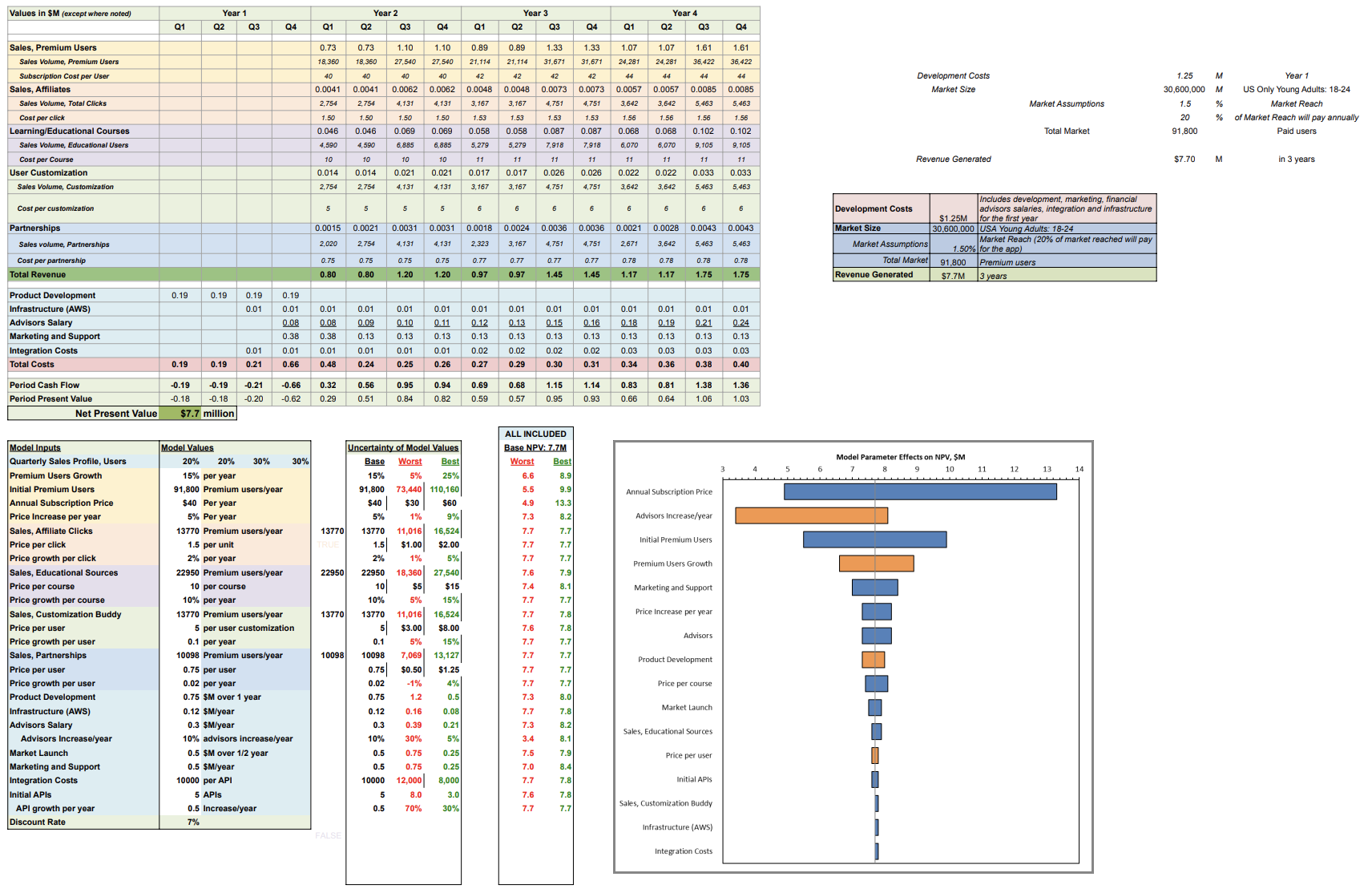

- performing competitive and financial analyses (NPV calculations)

- designing a prototype of the product solution

- presenting the solution to Steven Eppinger